Commercial Property Closing Costs: What to Know

While commercial property closing costs will vary depending upon the situation, and while closing costs should be outlined in the commercial mortgage terms, there are several common costs that an investor should be aware of. It’s important for an investor to understand all costs inherent with a loan, especially to ensure the ability to maximize leverage on an investment.

Different Types of Fees Involved with Commercial Property Closing Costs

A key factor to understanding commercial property closing costs is remembering that there are a variety of different fees at each stage of closing. A borrower should keep all common fees in mind when considering the return on any investment and add those fees into their calculations.

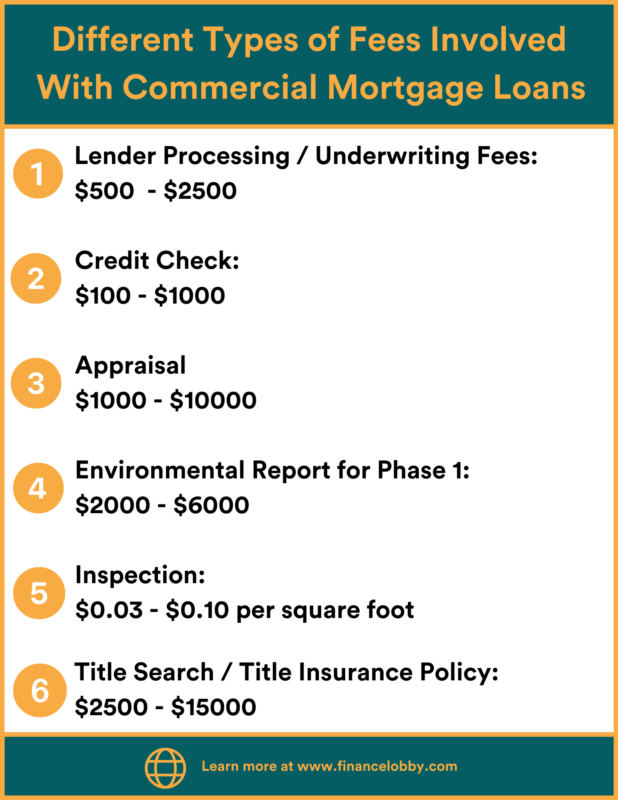

Lender Processing/Underwriting Fees: $500-2500

Mortgage lenders will typically charge fees for the time their staff spends underwriting and processing the commercial loan. This fee is often collected upfront via a deposit and should be outlined on the term sheet. This is a non-refundable fee. Commercial mortgage underwriting guidelines can be complicated so this fee is worthwhile for the investor.

Credit Check: $100-1000

The credit score of the borrower is extremely important in commercial real estate. A low credit score may mean that a lender is unable to complete the loan. Every stakeholder that is part of the transaction will need to undergo a credit check, so for multiple investors, the cost of credit checks will increase.

Appraisal: $1000-10,000

In commercial real estate, property information is key to securing a loan. A third party will need to assess and report on the condition and value of the property. This is absolutely required and non-negotiable for federally regulated financial institutions. Even for private lenders it’s a step almost always taken. The value given by the appraiser is determined by the size of the property, the location, and the type of property.

If an investor is looking to finance multiple properties in a portfolio, they will need to cover the appraisal costs for all properties involved.

Environmental Report for Phase 1: $2000-6000

For any commercial financing, it is required to have the property checked for any type of environmental issues. This includes the building or buildings and the land itself. If the property passes the inspector for the first phase environmental report, any problems can be immediately addressed. This will save time and money when entering Phase 2 of environmental inspections.

Inspection: $0.03-0.10 per square foot

A lender will order a physical inspection for a property to understand the condition of the building or buildings and the land. This will determine whether there is significant maintenance that will need to be done to bring the property up to code. Any kind of maintenance will require capital to fix, so this inspection determines how much capital will be needed to ensure the safety of the property. The cost of inspections usually depends upon the size of the property and what kind of property it is.

Title Search/Title Insurance Policy: $2500-15,000

A title company will handle calculations for title fees and will be the ones to disburse those payments upon closing. The title company will provide title insurance to the lender, as well as to any other parties involved in the transaction. Title insurance, in essence, is intended to protect the lender from losing out financially in case any claims are discovered against the title of a property. This can include a broker or contractor who will claim that they performed work for which they were not paid. The title company starts by performing a title search to discover any of these claims, and once any existing claims have been resolved, the transaction can move forward.

Mortgage Registration/Recording Tax: Depends upon location

In the United States, the rules and regulations regarding the recording of deed transfers, liens, and mortgages can vary depending upon the state or even the county. Mortgage recording may be a flat fee in certain places, usually totaling several hundred dollars. In other places, the mortgage recording fee will be a percentage of the loan amount and will be described as a mortgage registration tax.

Lender Origination Points: 0%-2%

Origination points are the fees charged for the evaluation, processing, and approval of mortgage loans, and for commercial mortgages, the fees vary depending upon the type of lender. Some lenders originate at “par”: this means they don’t charge points, but rather make money on the set interest rate.

Banks and credit unions, however, often charge 0.25%-0.5% of the loan amount. This is their origination fee. Private lenders may charge 2% or higher on more expensive assets and assets deemed high risk.

Commercial Mortgage Broker Fee: 0%-2%

When negotiating commercial financing options, a borrower may choose a commercial mortgage broker or platform. In this case, they will be assessed a fee. These brokers or platforms will usually see a fee of 1%-1.5% of the loan amount for arranging a small-balance commercial mortgage, which is typically less than $5 million USD.

Borrowers should research their broker before choosing one. Some brokers are trustworthy and experienced. However, some commercial mortgage brokers will try to claim fees both from the borrower and from the lender. This is considered unethical but is not always strictly illegal.

Lender’s Legal Fees

It’s not really possible to set a specific range on the legal fees for the lender because this can vary significantly depending upon the size of the loan. Legal fees can be upwards of $15,000 for commercial mortgage-backed security (CMBS) loans of, for example, under $5 million. This is partially due to the complexities of securitization. Larger loans may carry legal fees of $30-100,000 for larger loans.

CMBS loans usually carry the highest legal fees. A local bank or credit union may charge quite a bit less..

Borrower’s Legal Fees

The legal fees an investor is responsible for also vary depending on the complexity of a particular deal, the type of property, and the size of the loan. The borrower’s legal fees are usually much less than the lender’s as the lender is the party drafting documents.

Adding Up Your Commercial Property Closing Costs

While all these different types of fees are typical for standard commercial real estate mortgage loans, there can also be other miscellaneous expenses. These are usually smaller than other types of fees but everything adds up. For example, a borrower may need to plan several trips to view a property, and this can include expenses for hotels, gas, and other travel costs.

It’s also a good idea for a borrower to consider setting aside funds for things such as hiring consultants to assist them along the way while closing on a property. A borrower also might need to pay fees for things like getting a professional evaluation of a property. Say an investor wants to purchase a retail building but notices that the roof is leaking. They might need to pay a fee for an estimate from a professional roofer so they know how much it will cost to repair the roof.

Keeping Capital Available After Closing

It’s always advisable for a borrower not to spend all their available capital on the commercial property closing costs. Investors should keep cash reserves readily available as other costs may arise. Even if the borrower has already viewed the property, the unexpected could happen: a storm, fire, or flood could occur during closing, necessitating another visit to the property to assess the damage to see if they still want to purchase the property and how much the repairs might cost. This could mean even more travel expenses along with budgeting for additional repairs.

It’s not really possible for an investor to plan out every last dollar when it comes to estimating the commercial property closing costs. But it’s a good idea to keep a cash reserve when acquiring a property. Lenders will take a look at all the borrower’s assets, including whatever money they have leftover after paying all the fees for closing. They want to know that the borrower will be able to continue making payments after closing.

Also, a borrower needs to ensure that they have the available capital to actually run the business after closing on a commercial property. If an investor wants to open a restaurant, for example, and he spends every bit of his savings just buying the building, he won’t have anything left to buy inventory, equipment, hire staff, pay property taxes, pay utilities, or do any marketing in order to attract customers to his new restaurant! He also won’t even be able to make his mortgage payments. These are all things that lenders look at during the process of underwriting a loan and determining the commercial property closing costs.

Finance Lobby is an online CRE lending marketplace that is making it faster and more efficient for commercial real estate brokers and lenders to find their perfect deals. To learn more about Finance Lobby, please see https://financelobby.com/.